In a significant step towards making India a cashless economy, the government on Monday launched BharatQR code, which it is saying is the world’s first inter-operable payment solution.

Developed by National Payments Corporation of India (NPCI), Mastercard, and Visa, BharatQR code would require merchants to only display a single QR code instead of multiple ones. This is expected to make payments seamless for buyers as they just have to “scan to pay” for transactions instead of swiping their credit/debit cards.

Here is all you need to know about it:

What is BharatQR code?

QR code or Quick Response code is a two-dimensional machine-readable code made up of black and white squares and are used for storing URLs or other information.

These can be read by the camera of a smartphone.

Private e-wallet companies like PayTM, MobiKwik, Freecharge and Oxigen are already using QR codes to allow customers to make payments from mobile wallets.

How does it work?

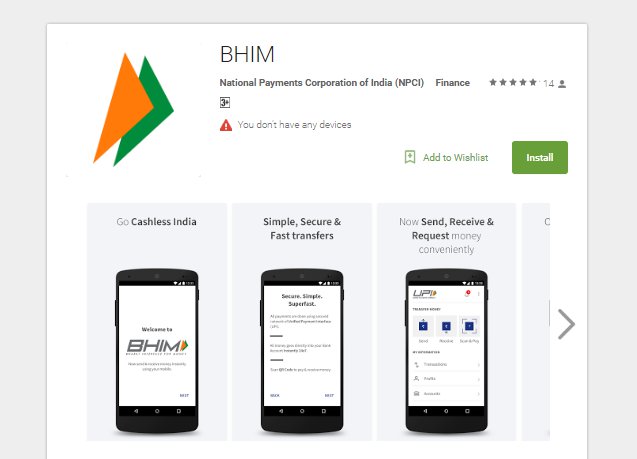

Shops have to first download BHIM app from Google Play store from a compatible Android or a iOS smartphone.

They have to then link it with their bank account after which a QR code will be generated.

The QR code will then be displayed at their shops. Customers can scan the QR code from their smartphones and the money will be deducted from their bank accounts which will directly go into the merchant’s account.

What are the benefits?

Merchants wouldn’t now have to install PoS machines to accept card-based payments. It will thus save them the cost of installing and maintaining them.

Payments using BharatQR will reportedly be comparatively safer than debit/credit card payments because several cases of card skimming/cloning have been reported in the recent times.

How is it unique from other QR code-based payment?

Private e-wallet companies like PayTM, Mobikwik, Freecharge also work on the same basis. But they have certain limitations as they don’t allow inter-operable payment solutions. For eg, a PaytM user can only transfer money to another PayTM user.

BharatQR code allows interoperability as the merchants will be identified by one QR code whether the payment is through MasterCard, Visa or RuPay.

Private e-wallet companies have another limitation. If one wants to transfer money from his/her e-wallet to the registered bank account, a transaction fee will be charged.

However, BharatQR allows one to directly transfer money to the bank account.

How many banks offer BharatQR?

A number of leading banks are already operationally ready to deploy BharatQR, including SBI, Axis Bank, Bank of Baroda, Bank of India, Citi Union Bank, Development Credit Bank, Karur Vysya Bank, HDFC Bank, ICICI Bank, IDBI Bank, RBL Bank, Union Bank of India, Vijaya Bank and Yes Bank.

Many other banks are at different stages of implementation.

What are the biggest problems?

Transactions wouldn’t be free of cost for merchants as they will still have to pay a merchant discount rate or MDR to the issuing bank every time a transaction is executed.

The BHIM app also has certain limitations. The transaction limit is Rs. 10,000 per transaction and Rs. 20,000 per day.

Users without smartphones or internet connectivity cannot use BharatQR code.

(With inputs from PTI)

(Feature image source: Twitter| Techno Geek)